Often times, I encounter buyers that have not obtained a pre-approval or even spoken to a lender because they do not want their credit to be adversely affected by an inquiry. Unfortunately, most agents will not take buyers around that have not been pre-qualified. Time and gas are expensive, and few agents will invest in a buyer that they are not certain will qualify for a mortgage. It is definitely beneficial to have at least a preliminary understanding of what you can qualify for up front to avoid a lot of wasted time and gas of your own. House hunting is fun and exciting up to a point, but the last thing you want to do is tour homes for several months in a specific price point that you think you can afford based on your monthly income, only to realize when you finally do speak with a mortgage lender, that you have not factored in the taxes, PMI and closing fees, and that you will actually only qualify for $100k less than anticipated. So getting pre-approved up front prior to house shopping is an excellent idea and an integral part of the process. And the best part is that a credit report is good for 90-120 days depending on the type of loan program. So once you are pre-approved, your credit does not have to be run again for another 3-4 months. By the time you are ready to purchase, the effect of the initial credit inquiry may not even be visible, and if it is, will have little to no effect on your score.

So what about when you want to rate shop and price out loan options? What impact does that have on your credit score? I have found that there is a lot of confusion and conflicting information circulating amongst consumers and even a few mortgage professionals regarding how running credit really impacts a FICO score, and naturally felt the need to do more research to clear up the confusion.

The one fact that is thus far undisputed is that there are two different types of inquiries. There are soft inquiries and hard inquiries. A soft inquiry is one that is for informational purposes only and does not accompany an entire credit report. It’s just an at-a-glance check of your score. For example, if you were to go on consumer sites like Credit Karma, that would generate a soft pull of your score. The downside of the soft pull is that it can often be misleading, inaccurate, and vary so much from a FICO that most lenders use to pre-approve you for a loan. In the credit repair industry, I’m told they are called “FAKE-Os.” Then there are hard inquiries, which are accompanied by a credit report. These are generated when you actually apply for any sort of credit. So each time you request a pre-approval from a bank, that is considered a credit application, they will make a hard inquiry on your credit in order to gain accurate data and will pull your report. That inquiry will not only show up on your credit report, it will have some impact, albeit minor, on your score. So what happens if you want to rate shop and call a lot of different lenders to get quotes? What’s great to know is that when shopping for mortgages, multiple inquiries made with different mortgage lenders within 45 days are considered duplicates and only count as 1 pull. That is actually federal law under the Fair Credit Reporting Act.

Having said that, this does not guarantee that your score will stay static for 45 days, it just means that it won’t be affected by multiple mortgage loan inquiries. 45 days is a big window of time in the credit reporting world, and your credit picture may alter in that time due to other influencing factors. Different industries report to the bureaus at different times within a given month, and debts and payments may pop up at varying points within the 45 day window that can alter your score, for better or worse. So your score may change in that 45 day window, and if it does it is for reasons entirely independent of the multiple mortgage credit inquiries. What’s also important to note is that the 45 day multiple credit pull rule applies only to car and house loans, and is industry specific. So if you’re shopping for both a car AND home loan, multiple inquiries related to both will be counted as 2 hard inquiries, one for each industry.

So how much does a hard pull really affect your score? The answer is that it apparently has a very minimal impact. Per the FICO website:

Fallacy: A score will drop if I apply for new credit.

Fact: If it does, it probably won’t drop much. If you apply for several credit cards within a short period of time, multiple requests for your credit report information (called “inquiries”) will appear on your report. Looking for new credit can equate with higher risk, but most credit scores are not affected by multiple inquiries from auto or mortgage lenders within a short period of time. Typically, these are treated as a single inquiry and will have little impact on the credit score.

Credit scores range from 300-850, but because FICO’s algorithm is proprietary, the numerical values contributed by each item reported on your credit report are not disclosed. So you can’t, for example, determine that a late payment will cost you x amount of points. It’s factored in, but you can’t calculate by exactly how much.

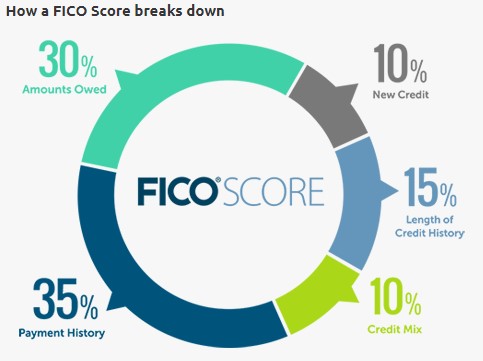

Fair Isaacs Corporation, better known as FICO, is the company that translates all the information collected from each of the three major bureaus and translates that into a number, or I should say 3 numbers – one for each bureau based on the information they provide. FICO basically programs the algorithm that analyzes the data and spits out the credit score. There are other companies that do it for educational purposes, for example, I mentioned Credit Karma, but FICO’s is the scoring system all lenders across the board use to determine credit worthiness. Per Fico, here is what goes into your credit score:

Certified FICO professional Eric Stuerken from Better Qualified, a credit building and monitoring agency, asserts “the impact from applying for credit will vary from person to person based on their unique credit histories. In general, credit inquiries have a small impact on one’s FICO Scores. For most people, one additional credit inquiry will take less than five points off their FICO Scores. For perspective, the full range for FICO Scores is 300-850. Inquiries can have a greater impact if you have few accounts or a short credit history.” He goes on to say that “FICO Scores ignore inquiries made in the 30 days prior to scoring. So, if you find a loan within 30 days, the inquiries won’t affect your scores while you’re rate shopping. In addition, FICO Scores look on your credit report for rate-shopping inquiries older than 30 days. However, for FICO Scores calculated from the newest versions of the scoring formula, this shopping period is any 45-day span.”

So in a nutshell, do credit inquiries affect your credit score? It’s a gray area. But it’s good to know that 1) if they have any effect, it’s minimal, and 2) multiple inquiries within a short period of time for a home or auto still only count as one inquiry. So what’s the takeaway? Go get yourself pre-approved. Rate shop. Do what you need to do, and do not be deterred by the minimal (if any) effect that a credit inquiry has on your report. You can’t make an offer without a pre-approval, and it’s difficult to find an agent willing to take you shopping without one either. Furthermore, it’s in your best interest to know what you can qualify for upfront to save you time, effort and tears down the road.

Sources: http://www.myfico.com

Contributers: Eric Stuerken, Better Qualified, President of Business Development; Matthew Fiorillo, Branch Manager, Movement Mortgage

Leave a comment